April brought mixed signals across U.S. natural gas markets. Prices moved lower, with prompt-month futures falling from about $3.02 to $2.77 per million British thermal units (MMBtu) over the course of the month, briefly touching an 18-month low near $2.63 mid-month. Strong domestic production averaging around 108 Bcf/day, healthy storage levels sitting roughly 8% above seasonal norms, and mild spring weather kept the U.S. market well-supplied and pressured prices lower throughout April. At the same time, global LNG markets remained tight as ongoing disruptions in the Strait of Hormuz continued to limit international supply, supporting strong export demand for U.S. gas. In short, the U.S. market exited April well-supplied and softer, while global supply risks continued to underpin international prices.

Bull Factors:

– Global LNG markets remained exceptionally tight as ongoing disruptions in the Strait of Hormuz continued to limit international supply. European and Asian gas benchmarks have risen roughly 48% and 83% respectively since tensions escalated in late February, meaning overseas buyers are paying a steep premium for cargoes. This widening price gap pulls more U.S. gas into export markets and supports long-term demand for domestic production, even though near-term U.S. prices remained subdued.

– U.S. LNG export demand stayed at near-record levels, averaging 18.9 billion cubic feet per day (Bcf/day) in April, up from 18.6 Bcf/day in March. When more domestic gas gets pulled into export terminals, less remains in the domestic system, which tightens balances and supports both natural gas and power prices over time. New export capacity is also coming online in the second quarter, including Corpus Christi Stage 3 and Golden Pass Train 1, which together add about 0.9 Bcf/day of capacity and reinforce the long-term demand floor for U.S. gas.

– Domestic production began to ease meaningfully, falling roughly 4 Bcf/day over an 18-day stretch in April to an 11-week low near 108 Bcf/day. The pullback was driven by economics rather than geology — with Henry Hub closing as low as $2.52/MMBtu on April 24, producing gas at full tilt became unprofitable in many basins. EQT, the second-largest U.S. gas producer, built 10 to 15 Bcf of production curtailments into its second-quarter guidance, framing the move as a way to “store supply in the ground” for peak summer power demand. The bigger picture is that producer discipline is returning to the market, which helps prevent further price erosion and sets the stage for tighter balances heading into summer when power burn for cooling demand ramps up.

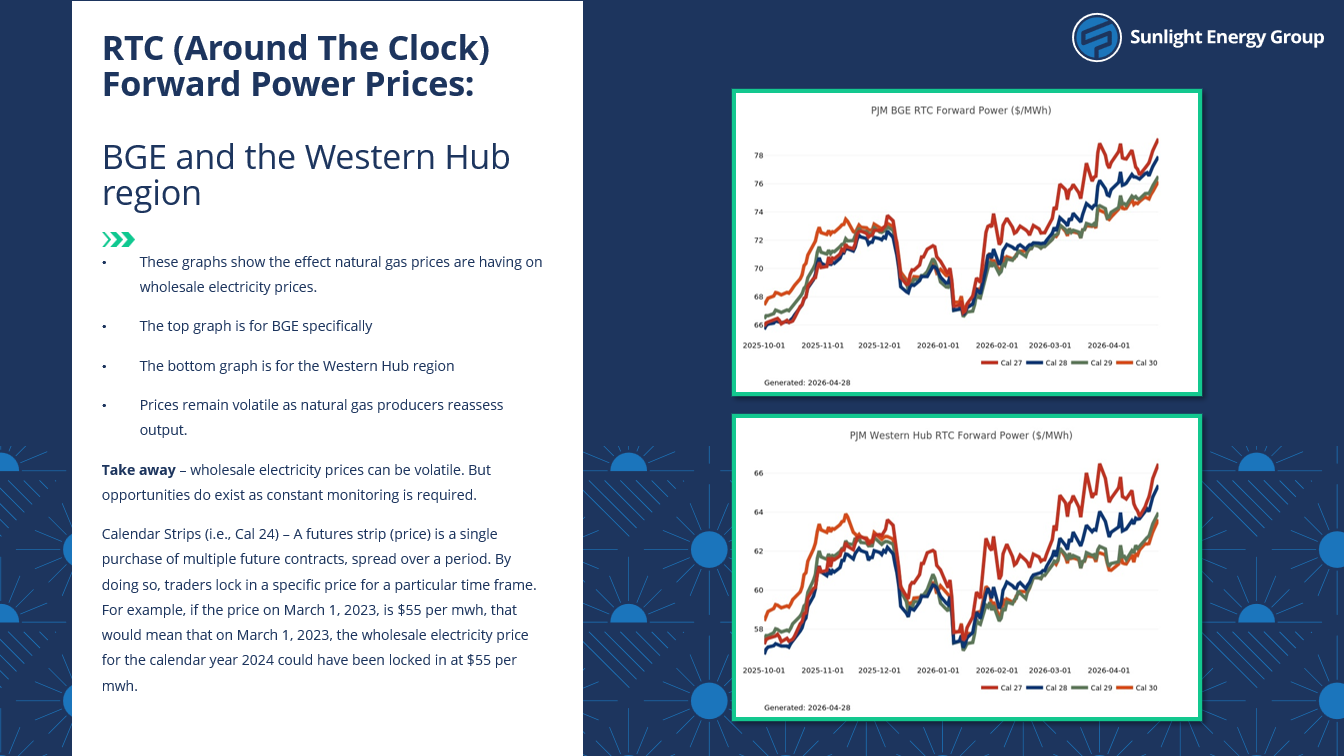

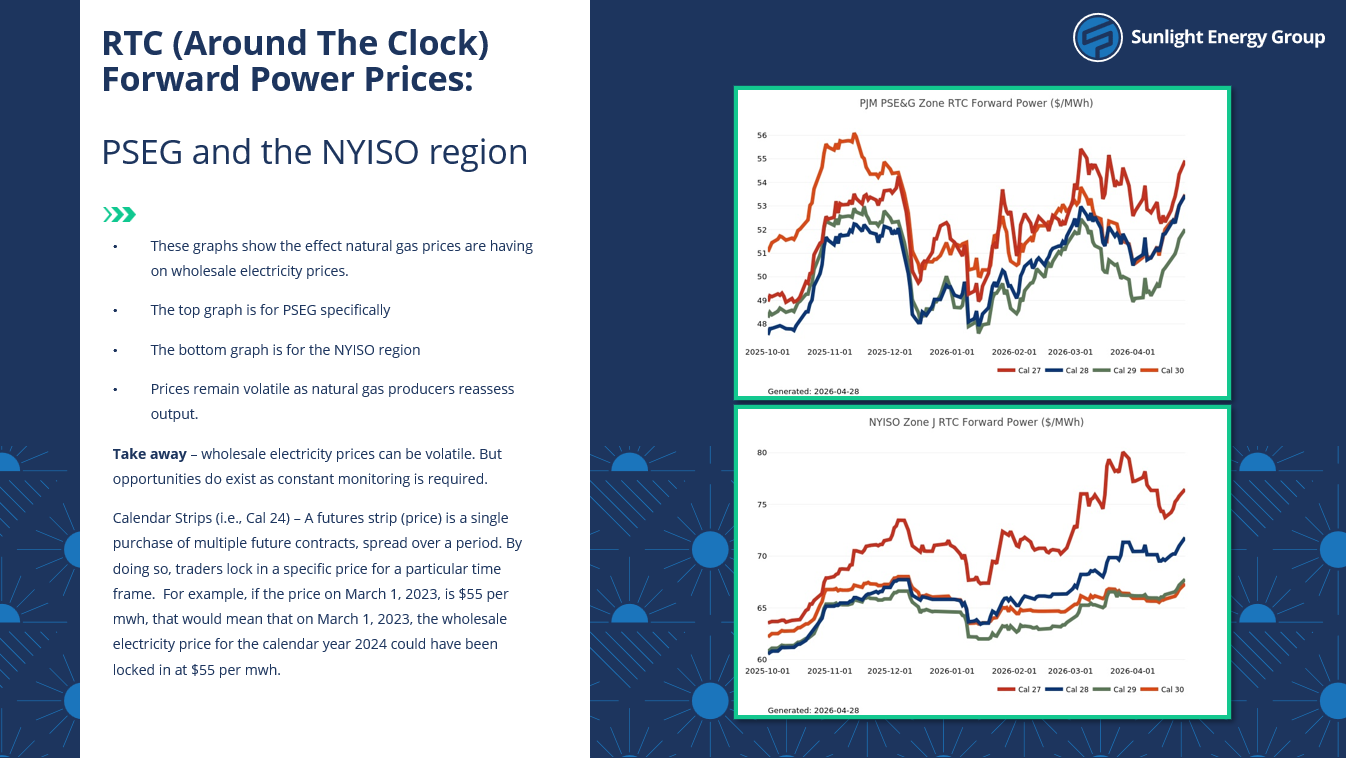

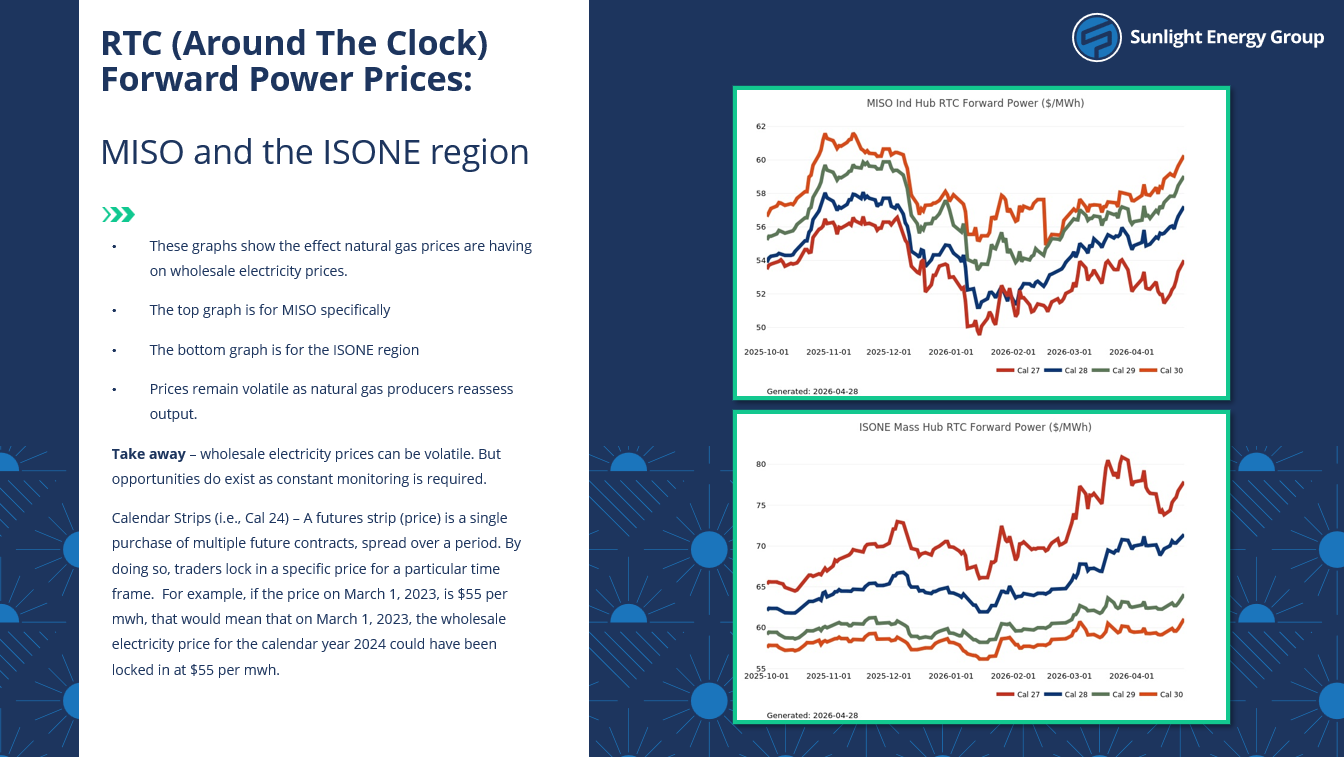

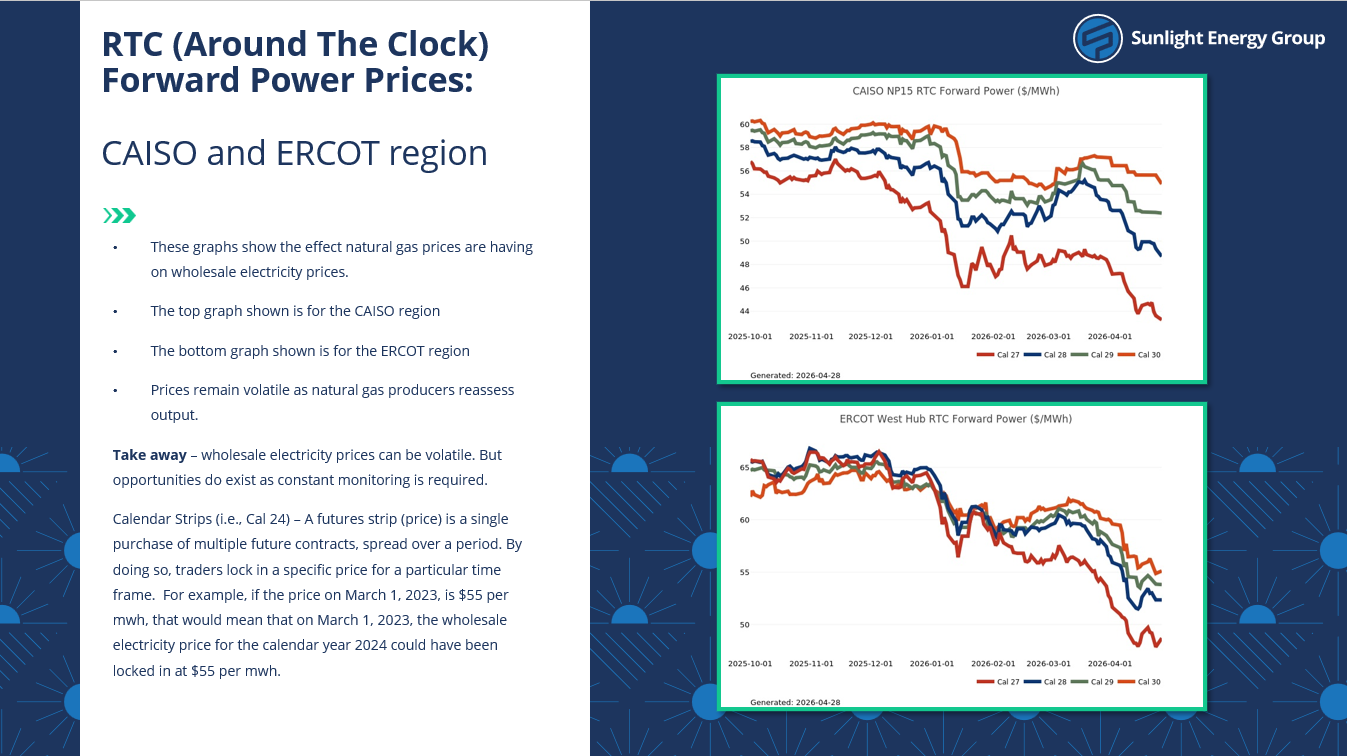

– U.S. electricity demand keeps growing, with sales projected to rise 2.6% in 2026. Commercial demand in Texas and surrounding states is expected to grow 17% this year alone, largely on data center expansion. When demand grows faster than new generation can be built, prices rise — which is exactly what’s playing out in PJM and ERCOT today and is likely to intensify as summer cooling load arrives.

Bear Factors:

– U.S. natural gas prices fell roughly 8% over the course of April, with futures hitting an 18-month low near $2.63/MMBtu mid-month. Despite tight conditions overseas, U.S. export terminals are running at near-maximum capacity and cannot ship out additional volumes, so domestic prices stayed disconnected from the global rally. The result was a well-supplied U.S. market with limited near-term price support.

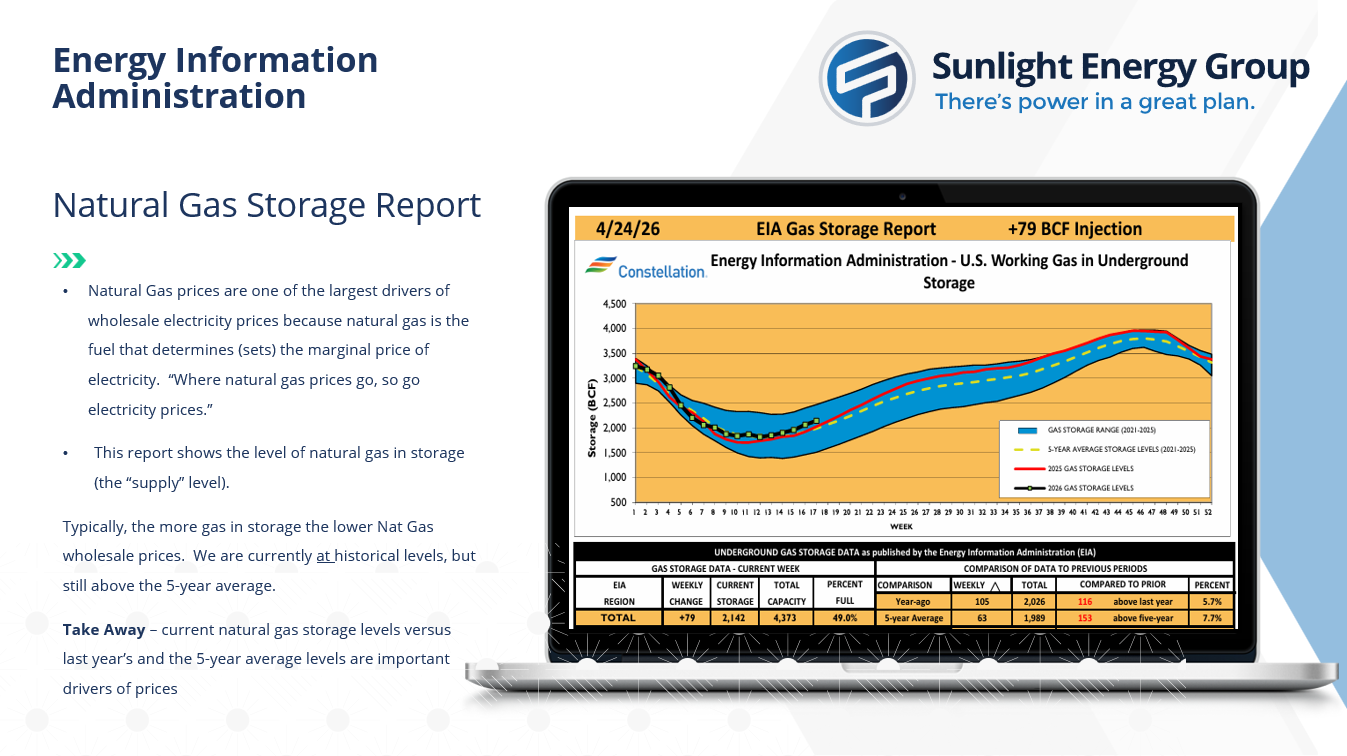

– Storage builds came in well above normal. The EIA reported a 103 Bcf injection for the week ending April 17, well above both last year’s 77 Bcf build and the five-year average of 64 Bcf. Inventories sat about 8% above seasonal norms by late April. When storage is comfortably full, the market feels less urgency about supply, which weighs on prices.

– Mild spring weather kept demand soft on both ends. Above-normal temperatures eliminated leftover heating demand while cooling demand has yet to kick in, creating a seasonal lull where natural gas consumption is naturally weakest. Forecasts for slightly cooler temperatures into early May are not expected to meaningfully change the picture.

Final Takeaways:

April highlighted a clear split in U.S. energy markets. Natural gas weakened on strong production, healthy storage, and mild weather, even as global LNG markets stayed extraordinarily tight on Middle East disruptions. The reason these global pressures didn’t lift U.S. prices is straightforward: export capacity is effectively maxed out, so additional global demand simply can’t reach U.S. supply right now. Power markets, by contrast, kept moving higher. According to the EIA’s Short-Term Energy Outlook, wholesale prices at the ERCOT North hub in Texas are projected to rise roughly 45% in 2026, while PJM’s annual capacity auction cleared 22% higher than the prior year and full-year wholesale market value rose 56% to $80.5 billion in 2025 (PJM Independent Market Monitor). EIA also reported retail electricity prices rose 9.0% nationally year-over-year in February 2026, with the Northeast and California seeing the steepest increases. Looking ahead, near-term natural gas prices may stay soft on comfortable supply and shoulder-season demand, but growing LNG exports and steady power sector demand should provide support over time. For power buyers, the message is the opposite, expect continued upward pressure through the summer, particularly in Texas, the Mid-Atlantic, and the Northeast, as cooling demand and data center growth keep the market tight.

Charts and graphs sourced from Constellation