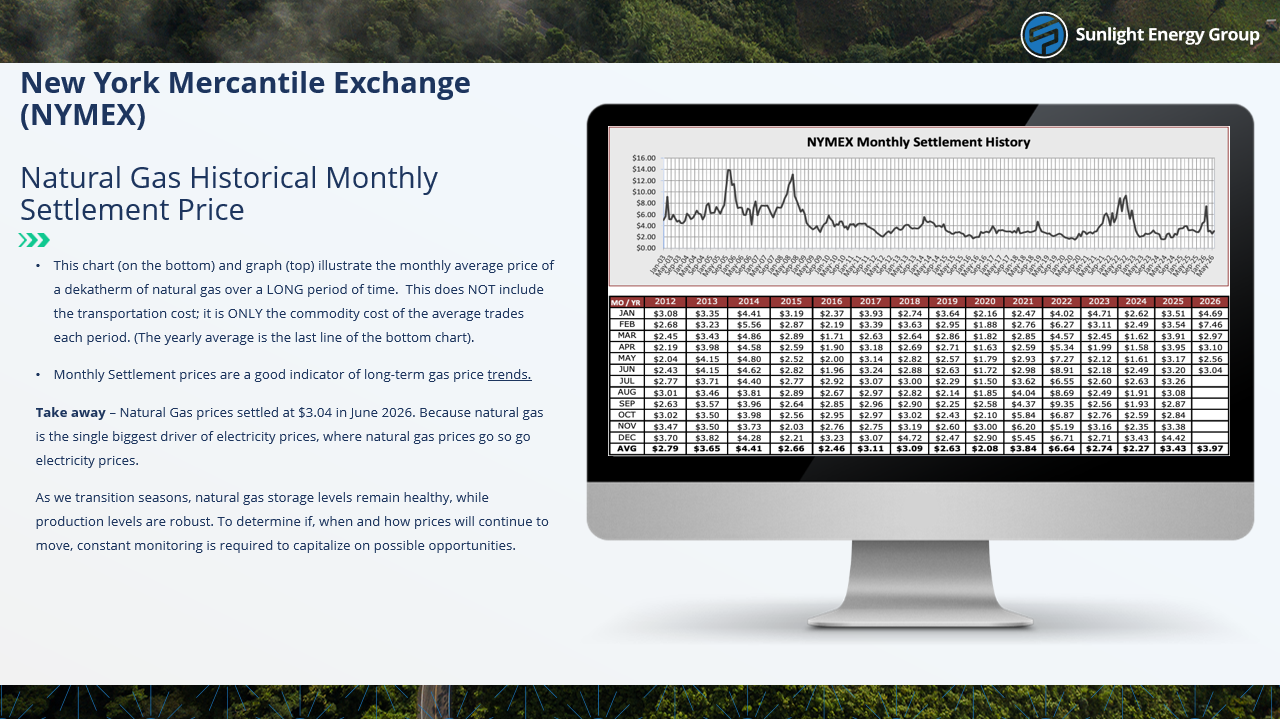

May brought continued mixed signals across U.S. natural gas markets, but with the first signs of a tentative price recovery. Prompt-month futures started the month around $2.66 per million British thermal units (MMBtu) and climbed steadily to roughly $3.10 by May 26, an increase of about 16% from the early-month low. Despite the rebound, Henry Hub spot prices remained generally below $3/MMBtu, a level the market hasn’t sustainably broken above since mid-March, and nearly 62% lower than the near-term high set on January 28. Strong domestic production resilience, storage injections continuing to outpace seasonal norms, and mild shoulder-season demand kept the U.S. market well-supplied throughout most of May. Globally, the Strait of Hormuz disruption entered its third month with no clear path to de-escalation, continuing to limit international LNG supply and supporting strong export demand for U.S. gas. In short, the U.S. market exited May well-supplied but firming, while global supply risks continued to underpin international prices.

Bull Factors:

– Global LNG markets remained structurally tight as the Strait of Hormuz disruption stretched into its third month. Tanker traffic through the strait is down roughly 90%, and repairs to Qatar’s damaged Ras Laffan facility, the world’s largest LNG export hub, could take up to five years per QatarEnergy. That means roughly 20% of global LNG supply will stay offline well beyond any near-term ceasefire. For U.S. markets, this sustains a heavy international pull on American gas exports, which tightens domestic balances and pressures both natural gas and power prices higher over time.

– U.S. LNG export capacity continued to expand. Golden Pass LNG Train 1 (0.7 Bcf/day) shipped its first cargo on April 22, with Corpus Christi Train 6 coming online this summer and Port Arthur, Rio Grande, and the final Golden Pass train expected next year. For U.S. markets, every new export train permanently raises the floor on domestic demand by pulling more gas out of the U.S. system, which is a key reason both EIA (Energy Information Administration) and the futures market expect higher prices in 2027 than today.

– Domestic producer discipline continued. Output remained noticeably softer than late-2025 peaks as Appalachian producers, led by EQT, kept curtailments in place to “store gas in the ground” for higher-priced summer and winter delivery windows. For U.S. markets, this means producers are refusing to flood the system with cheap gas, which puts a floor under prices today and accelerates the expected tightening as peak demand season approaches.

Bear Factors:

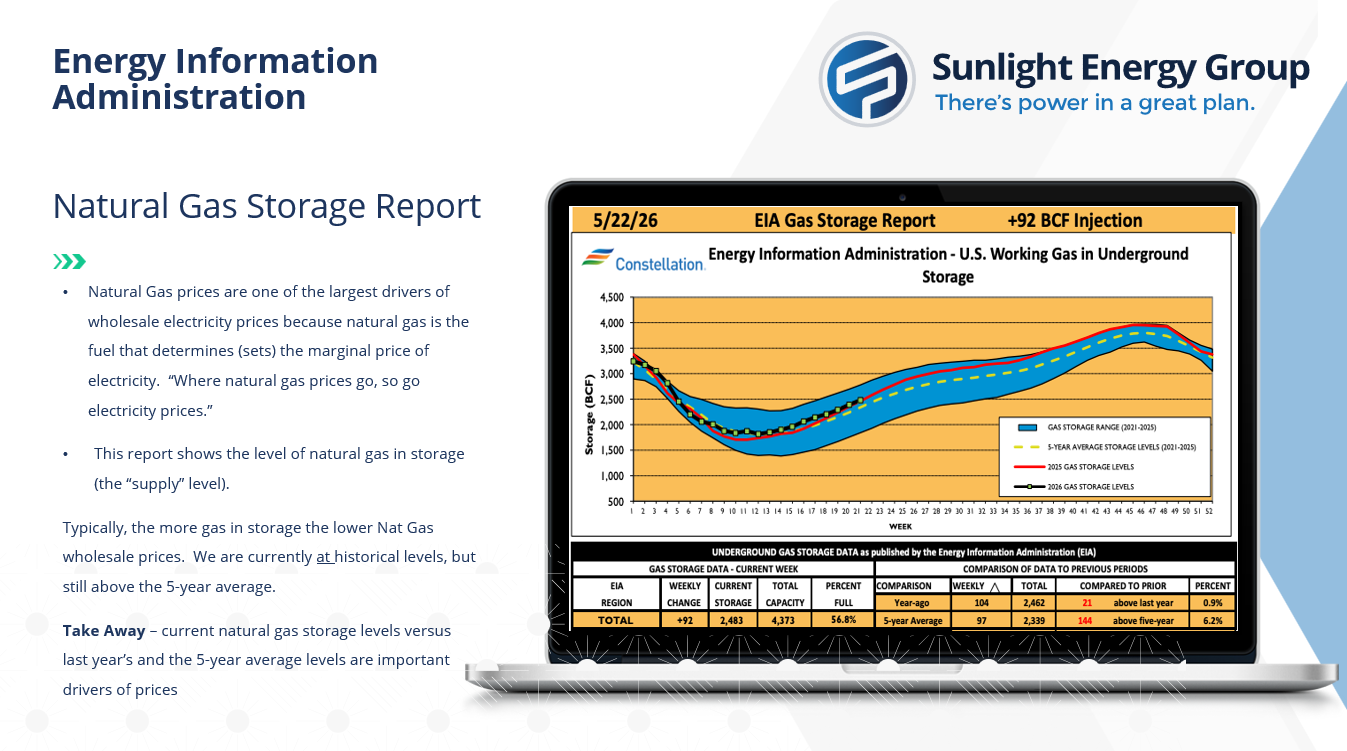

– Underground storage levels remain healthy and continue to build faster than normal. Inventories ended the winter heating season at 1,908 billion cubic feet (Bcf), about 4% above the five-year average, and the EIA now expects storage to finish the April–October injection season roughly 7% above the five-year average. For U.S. markets, storage is essentially the country’s natural gas savings account, and when it fills faster than usual the market feels less urgency about supply. That directly pressures near-term prices lower and softens power prices in regions where gas is the dominant fuel for electricity.

– Mild shoulder-season weather continued to suppress demand. Cumulative cooling degree days (CDDs) from April 26 through May 9 came in notably below normal, meaning cooling demand has yet to ramp up. For U.S. markets, weak shoulder-season demand means more gas flows into storage instead of being burned, which compounds the well-supplied picture and limits how much prices can rise until summer heat arrives.

Final Takeaways:

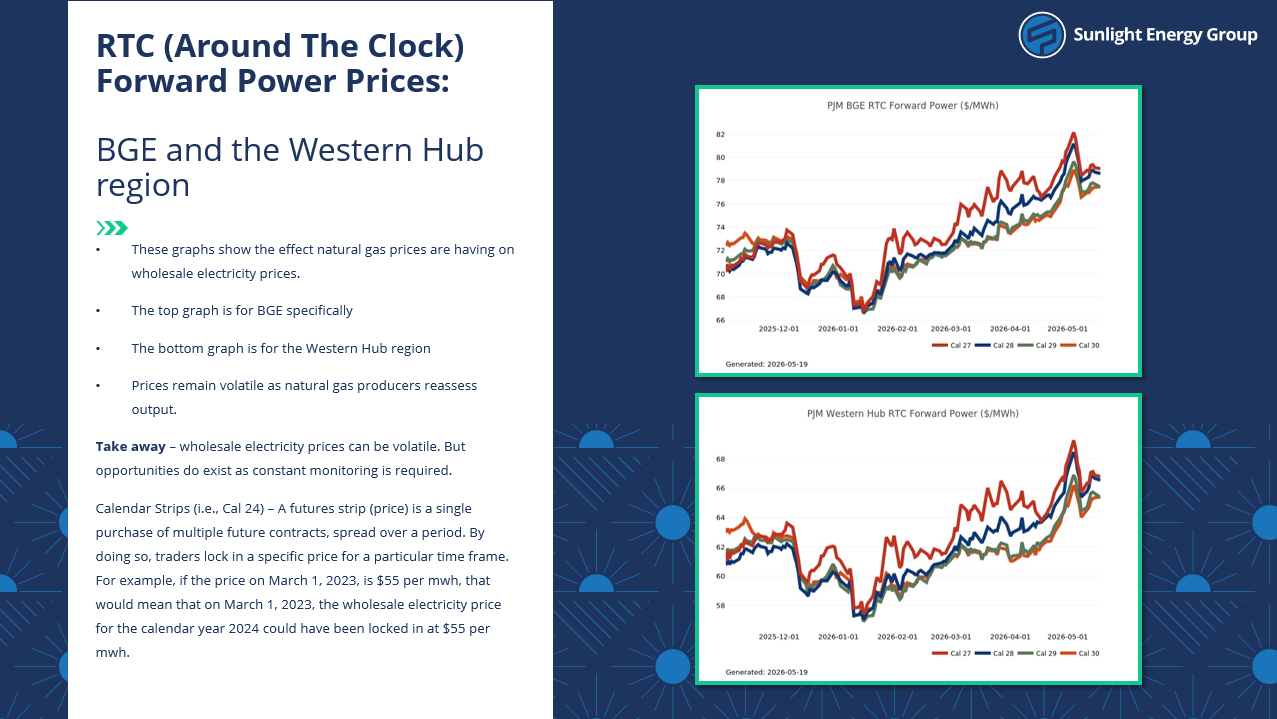

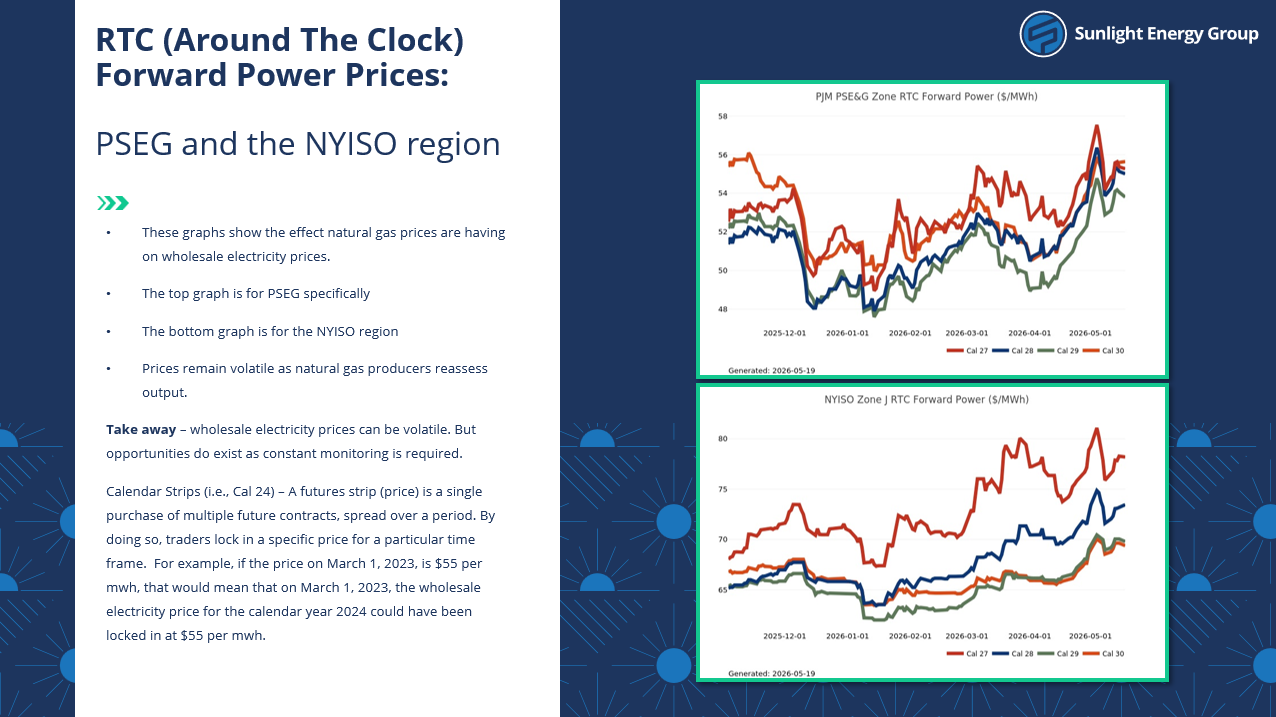

May marked a transitional month for U.S. energy markets. Natural gas prices began to recover from April’s 18-month lows, but the rebound was modest and the market remained fundamentally well-supplied in the near term. The combination of healthy storage, mild weather, and seasonal LNG maintenance kept a lid on price gains, even as the Strait of Hormuz disruption stretched into its third month and continued to support international prices. Power markets continue to tighten. Electricity demand is growing faster than new power plants can be built, especially in Texas and the Mid-Atlantic where data centers are consuming huge amounts of power.

Sources: U.S. Energy Information Administration (Short-Term Energy Outlook, May 2026); American Gas Association (Natural Gas Market Indicators, May 15, 2026); Utility Dive; QatarEnergy.

Charts and graphs sourced from Constellation