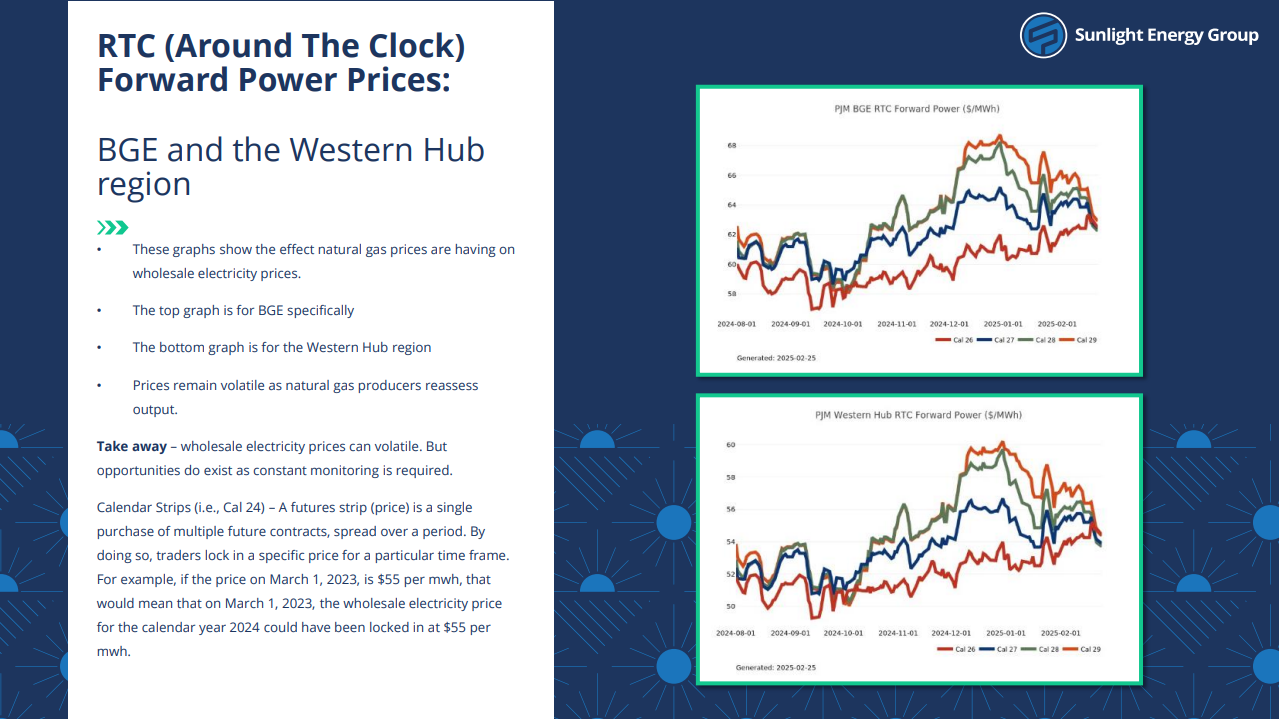

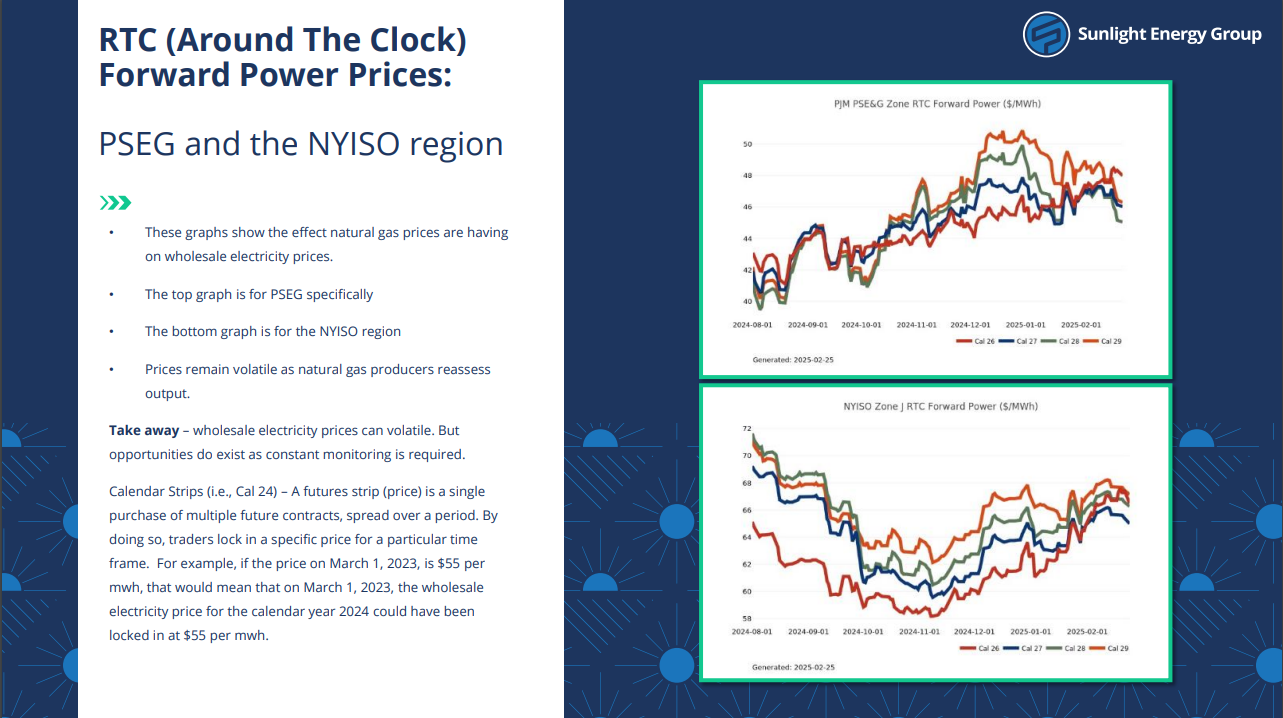

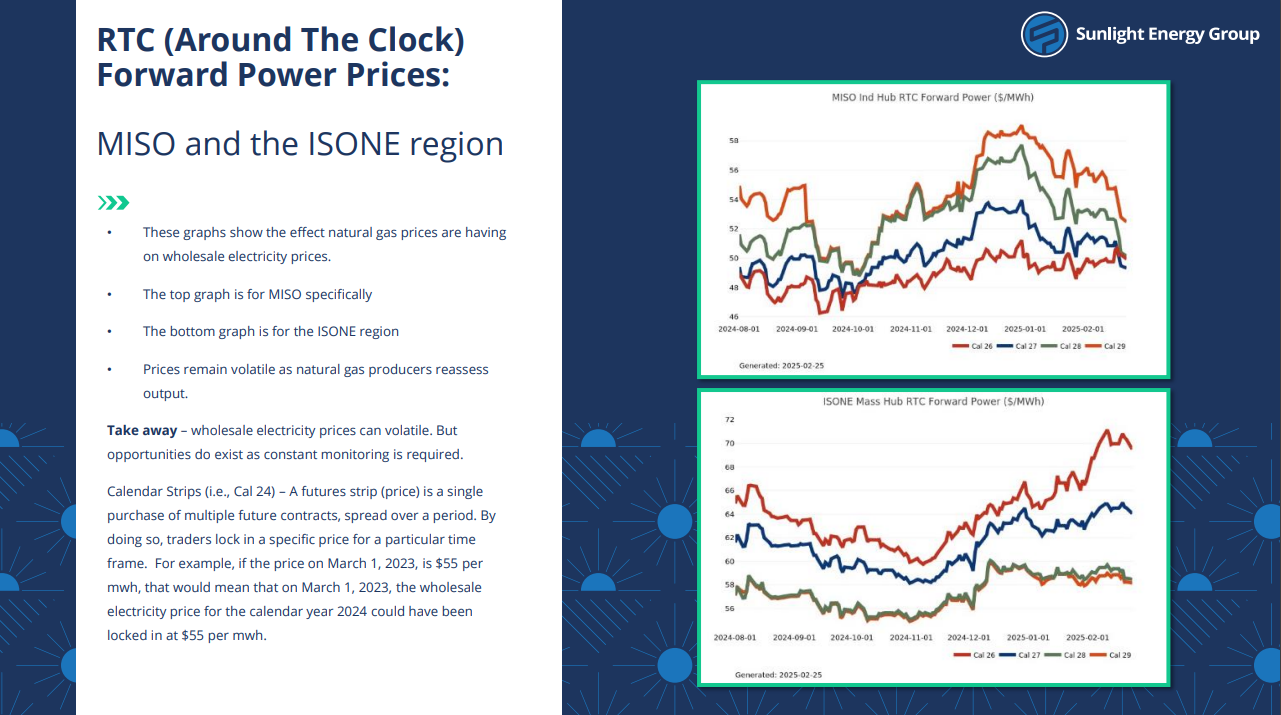

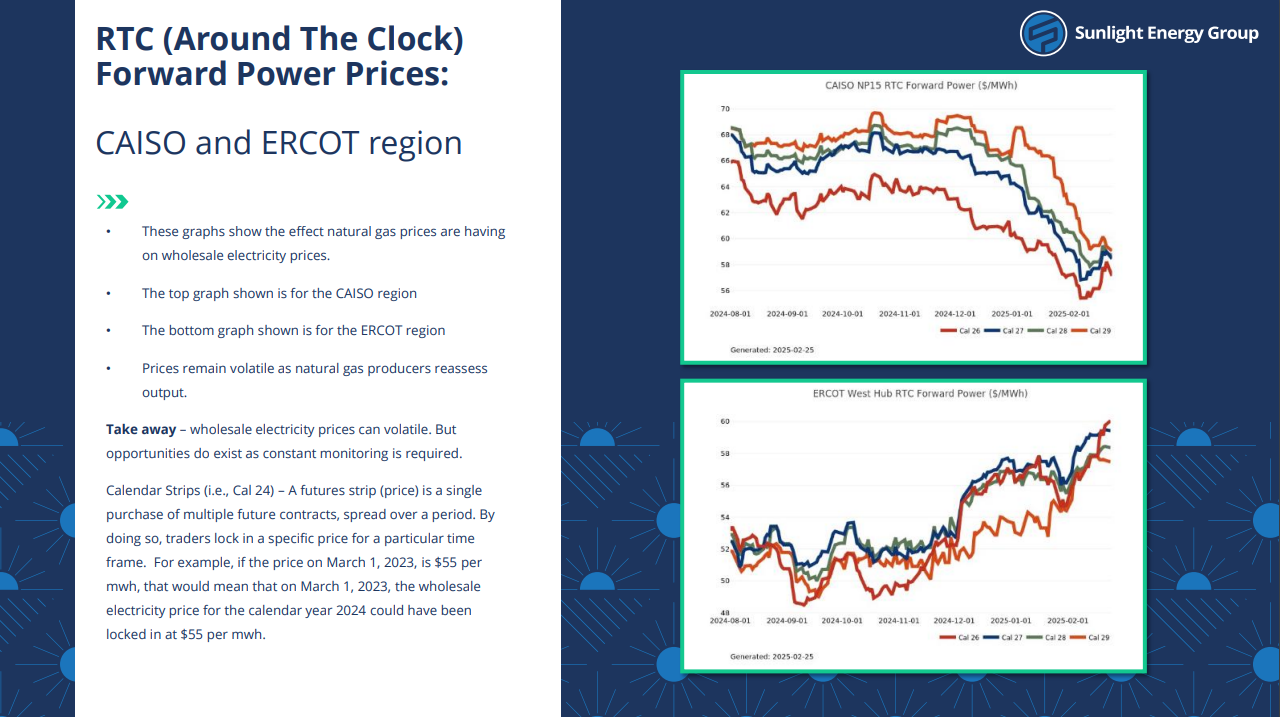

February saw persistent cold weather driving up natural gas demand, while crude oil prices remained stable despite geopolitical developments. End-of-season natural gas storage inventories fell to 2,101 Bcf (billion cubic feet), which is 118 Bcf below the five-year average and 386 Bcf lower than last year. Despite strong consumption, U.S. dry gas production reached 106.2 Bcf/day, and a seasonal transition to spring may ease market tightness.

NYMEX natural gas settled today at $3.93/MMBtu, down $0.06 from the previous day. While demand remains strong, prices have struggled to gain traction due to ample production and expectations of warmer weather ahead.

Bull Factors:

– Strong Natural Gas Demand: Residential/commercial demand averaged 48.3 Bcf/day, up from 41.0 Bcf/day last year, keeping upward pressure on prices despite seasonal shifts.

– Storage Deficit: Inventories at 2,101 Bcf, 118 Bcf below the five-year average, indicating a tighter supply situation that could support prices.

– Geopolitical Uncertainty: U.S. sanctions on Iranian oil, Keystone XL discussions, and U.S.-Russia talks underway, increasing supply risks that may create volatility in crude oil and refined product prices.

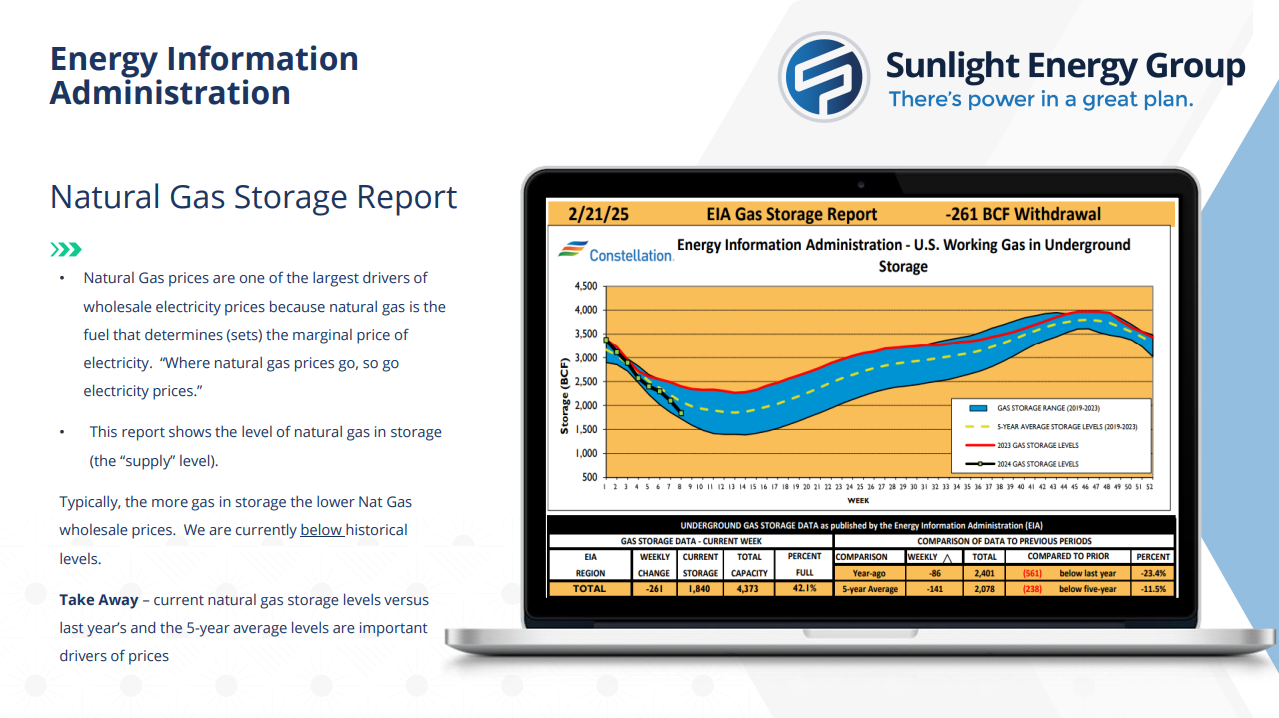

– Extended Winter: Cold temperatures persisted, with a 261 Bcf withdrawal from storage for the week ending Feb. 21, delaying the seasonal decline in natural gas prices

Bear Factors:

– Economic Headwinds: No near-term Fed rate cuts, home sales fell 4.9% in January, and hiring remains sluggish. Slower economic growth may weaken industrial energy demand, limiting natural gas price support.

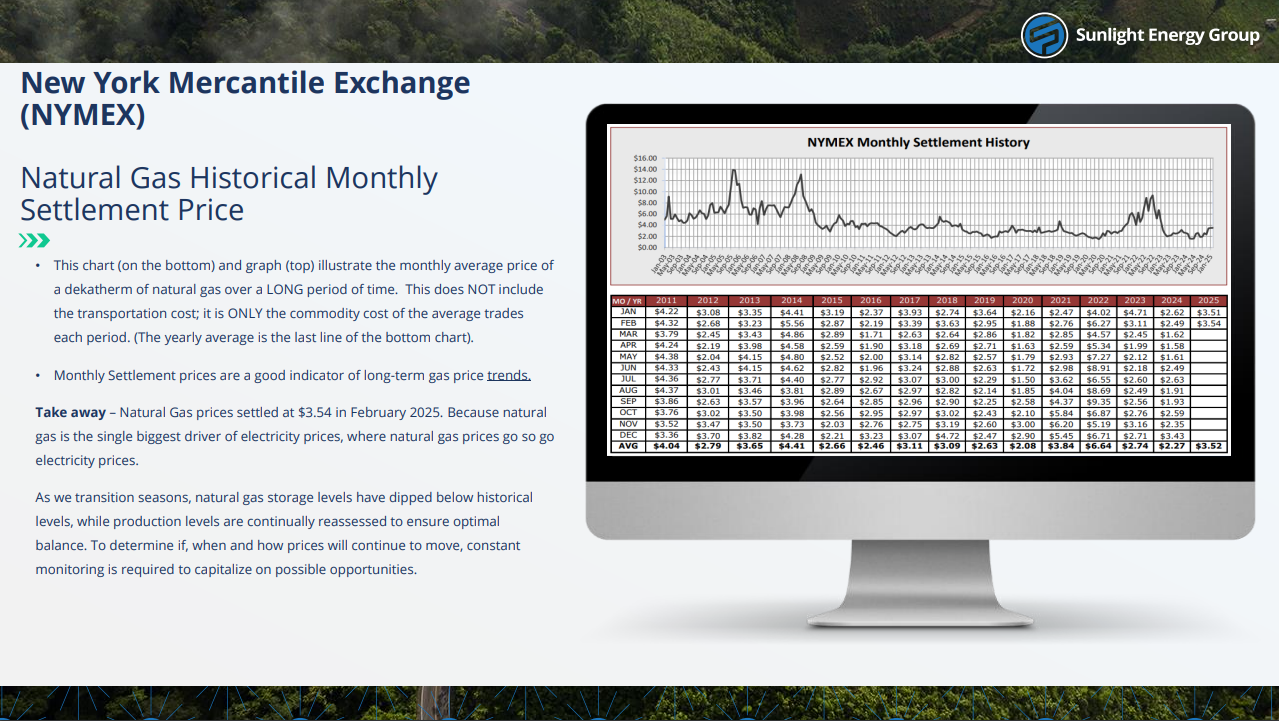

– Crude Oil Market Pressure: NYMEX (WTI) crude settled at $70.70/bbl, with OPEC’s 4+ million bpd spare capacity capping prices. Lower oil prices discourage drilling cutbacks, keeping associated gas production steady and natural gas supply ample.

– Supply Growth: U.S. dry gas production remains strong at 106.2 Bcf/day, increasing 0.7 Bcf/day day-over-day. Rising supply levels are helping offset storage deficits and putting downward pressure on natural gas prices.

– Warming Trend Emerging: Forecasts show above-average temperatures moving eastward, signaling lower heating demand. As winter demand fades, natural gas consumption is expected to decline, which could weigh on prices in the coming weeks.

– LNG Export Growth Stabilizing – LNG feedgas demand averaged 15.0 Bcf/day, up slightly from 13.8 Bcf/day last year. While short-term growth has leveled off, long-term demand for U.S. LNG remains strong as new export capacity is expected to come online, expanding market opportunities.

Final Takeaway:

While low storage levels and strong winter demand have supported prices, the market is nearing a transition. U.S. dry gas production remains high at 106.2 Bcf/day, and LNG exports have stabilized, helping offset supply concerns. Warmer temperatures are moving eastward, signaling lower heating demand, while economic uncertainty and ample crude supply could further weigh on prices. The next few weeks will determine if storage deficits keep prices supported or if rising production and seasonal shifts lead to a more balanced market.

Charts and graphs sourced from Constellation