April 2025 reflected a stable but nuanced natural gas market, shaped by strong production, elevated LNG export volumes, and above-average storage injections that were well-absorbed by the system. Natural gas prices ended the month at $3.17/MMBtu, with a $0.23 gain on April 28, largely driven by a combination of technical buying and tightening near-term balances. While supply remained near record highs, increased exports and steady domestic demand helped limit downside pressure. Crude oil prices trended lower throughout the month, influenced by expectations of increased global supply and soft macroeconomic indicators. Overall, market conditions pointed to a system in relative balance, with neither oversupply nor demand weakness dominating the landscape.

Bull Factors:

– LNG exports were strong and consistent throughout the month. U.S. LNG exports averaged 16.0 Bcf/day in April, up from 11.8 Bcf/day during the same period last year. Contributing to this strength was the recovery of the Corpus Christi LNG facility, which returned to full service following a brief outage earlier in the month. These export volumes played a key role in tightening the domestic supply balance by redirecting gas away from storage.

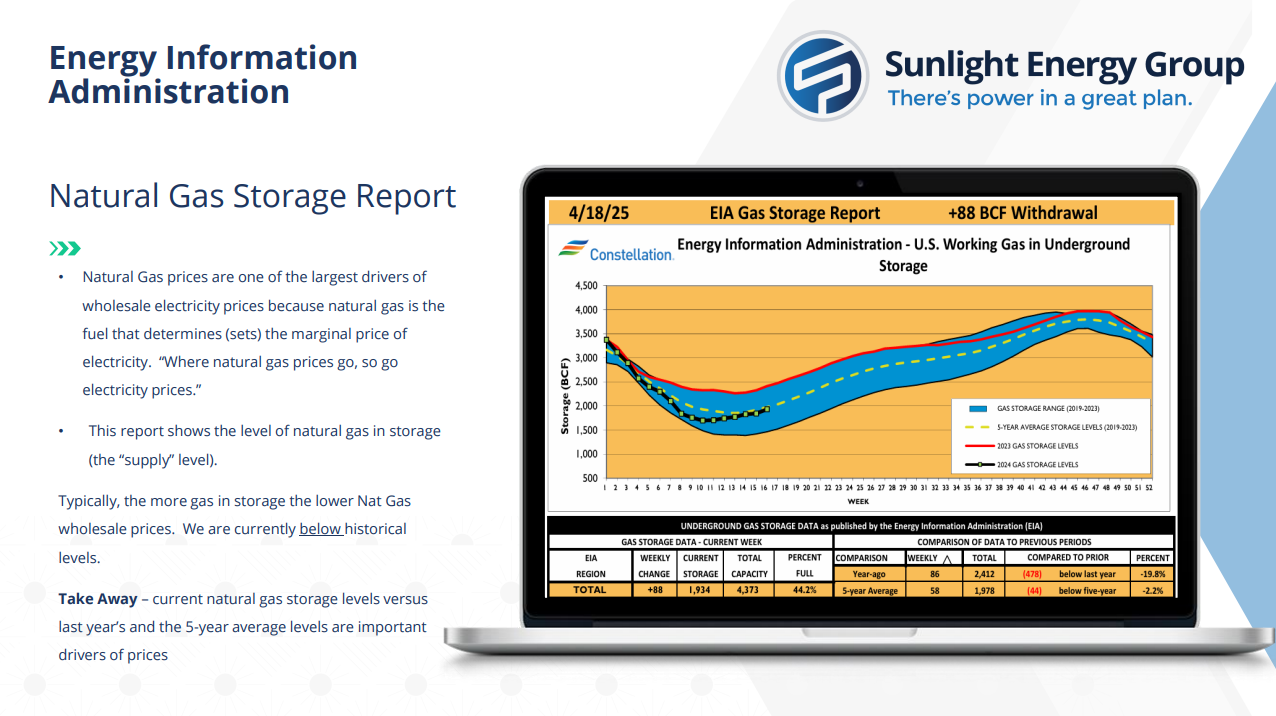

– Storage injections exceeded seasonal averages without softening prices. The 88 Bcf injection for the week ending April 18 was well above the five-year average of 58 Bcf. Despite the sizable build, pricing remained firm, suggesting that supply growth is being met with sufficient demand and off-system movement.

– Production remained elevated but was met with sufficient demand. Natural gas production averaged 105.0 Bcf/day during April—up from 99.9 Bcf/day last year—with recent daily highs exceeding 106 Bcf/day. This output level has not led to excessive storage builds or sharp price declines, indicating equilibrium between supply and demand.

– Weather forecasts pointed to a warmer-than-average summer. Multiple seasonal outlooks indicate the potential for above-normal temperatures across much of the U.S. this summer. While not expected to be extreme, warmer conditions historically lead to increased electricity demand for cooling, which can raise natural gas consumption for power generation in regions reliant on gas-fired units.

Bear Factors:

– Electric power demand for natural gas declined year-over-year. April power burn averaged 28.5 Bcf/day, down from 29.5 Bcf/day in 2024. This reduction reflected mild spring temperatures and increased use of renewables, which displaced some gas-fired generation.

– Macroeconomic indicators pointed to slowing momentum. U.S. jobless claims rose to 220,000, while March housing starts declined by 11.4%. These metrics suggest tempered economic activity, which can influence broader energy consumption across commercial and industrial sectors.

– Crude oil prices continued trending lower. WTI settled at $61.87/bbl on April 28 amid global demand concerns and potential supply growth. Sustained low oil prices can slow drilling in oil-rich basins like the Permian, which may reduce associated gas output and tighten natural gas supply over time.

– OPEC+ signaled potential production increases. Indications of higher output from key OPEC+ members have added downward pressure on oil prices. If realized, lower oil revenues could lead to reduced U.S. shale activity, indirectly curbing associated gas production that feeds into domestic natural gas supply.

Final Takeaways:

April data reflected a well-supplied natural gas market that remained fundamentally supported by strong LNG exports, elevated production, and restrained storage growth. Crude oil markets, by contrast, faced consistent downward pressure driven by supply-side uncertainty and softening economic signals. As the calendar turns to May, markets continue to reflect real-time supply and demand dynamics, with no single factor exerting dominant influence.

Charts and graphs sourced from Constellation