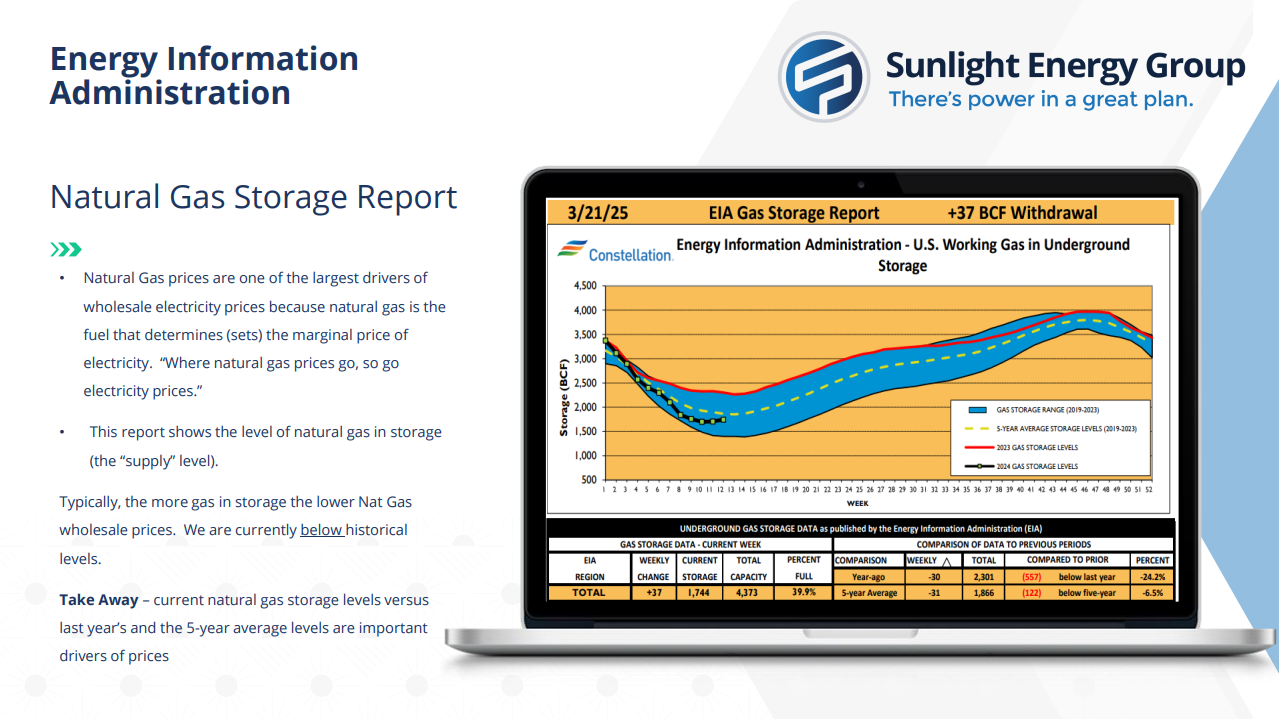

Underground natural gas storage levels remain well below historical norms, with inventories at 1,707 Bcf (billion cubic feet) as of March 14 — 624 Bcf lower than last year and 190 Bcf below the five-year average. This tighter storage position typically supports prices, but in March, other market forces kept natural gas values in check.

Natural gas prices eased slightly this month, with NYMEX prompt-month gas settling at $3.91/MMBtu, down $0.07. Warmer seasonal weather and rising production softened the market, despite strong year-over-year demand and export activity.

Bull Factors:

– Year over year demand growth: LNG (Liquified Natural Gas) exports rose to 15.2 Bcf/day (from 13.4 Bcf/day last year), indicating strong international appetite for U.S. natural gas, which draws down domestic availability. Residential/commercial demand increased to 41.7 Bcf/day (from 35.1 Bcf/day), reflecting a colder early-season and broader usage. Electric power generation usage also climbed to 33.6 Bcf/day, up slightly from 32.8 Bcf/day, signaling stable baseload demand.

– Lower storage levels: Gas in storage is well below both year-ago and five-year benchmarks. Inventories stood at 1,707 Bcf, which is 624 Bcf below this time last year and 190 Bcf below the five-year average. Tighter inventories reduce supply flexibility and can increase price volatility, especially if demand spikes unexpectedly.

– Macroeconomic factors provided some support: The U.S. dollar weakened, which often pushes commodity prices higher as they become cheaper for foreign buyers. Although the Federal Reserve held interest rates steady, some policymakers hinted at future rate cuts, which may encourage investment and consumption—potentially boosting energy demand.

Bear Factors

– Natural gas production remains elevated: Month-to-date average production is 104.8 Bcf/day, up from 101.8 Bcf/day a year ago. Elevated production can cushion price movement as well as place downward pressure.

– Seasonal weather reducing urgency in the market: After a brief cold snap, weather models show a general warming trend extending through April. This has dulled the weather’s impact as a price driver and reduced short-term heating demand.

Final Takeaways:

While natural gas storage remains low and overall demand metrics are stronger than last year, increased production and a mild weather outlook have capped upside momentum for now. Crude oil gained on geopolitics and currency movements, but both markets face uncertainty from macroeconomic and trade-related developments. As the industry enters spring, attention shifts to storage injections, summer forecasts, and global economic signals to determine the next move in energy pricing.

Charts and graphs sourced from Constellation