The energy market continues to show a blend of bullish and bearish dynamics as we close out the year, with production, demand, and storage levels playing key roles in shaping the natural gas outlook. While bullish signals include increasing demand for electric power and robust LNG exports, bearish factors such as above-average storage levels temper upward price momentum. The January ’25 natural gas price closed at $3.514 per MMBtu last Friday. December saw significant price swings, with lows of $3.042 per MMBtu and highs reaching $3.946 per MMBtu, reflecting notable market volatility throughout the month.

Below is a categorized summary of some key market drivers:

Bear Factors:

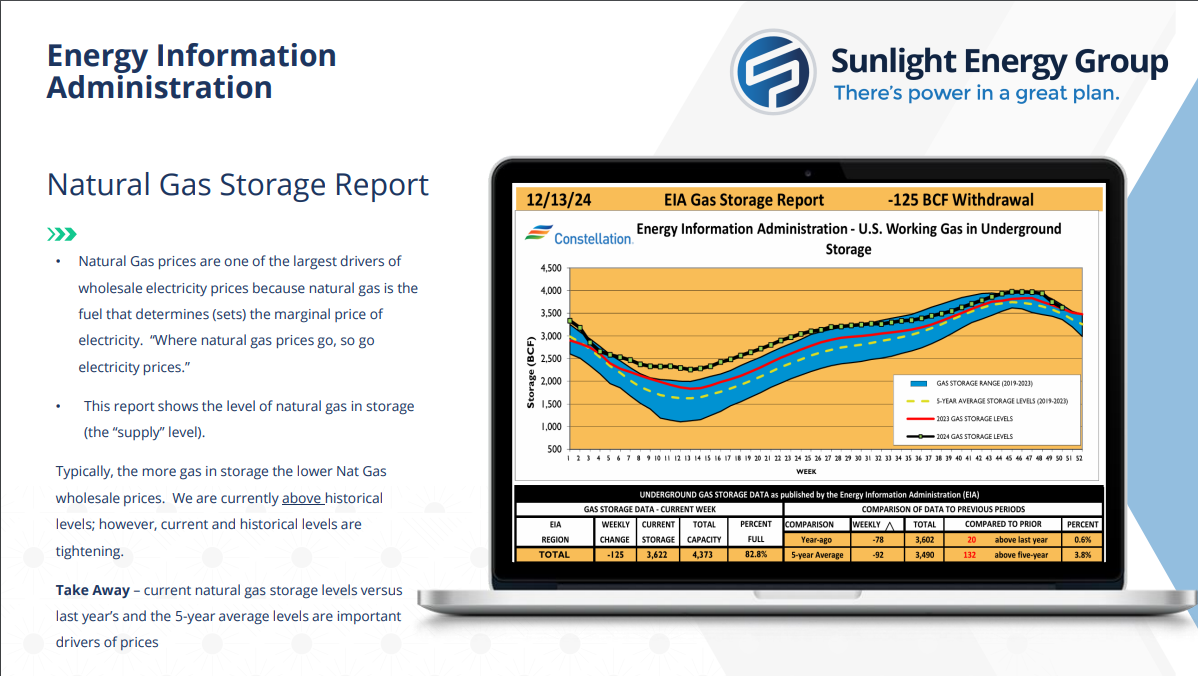

– Natural gas storage levels the week ending December 13th sits at 3,622 Bcf (billion cubic feet) which is 20 Bcf above last year’s levels and 132 Bcf above the 5-year average levels. Healthy storage levels have allowed prices to remain somewhat stable as seasonal demand hits.

Bull Factors:

– Natural gas production month-to-date averaged 103.9 Bcf/day, slightly below last year’s 104.8 Bcf/day, indicating stable supply levels. Natural gas producers are consistently adjusting their production levels in order to address the surplus of natural gas.

– Electric power generation demand increased to 34.9 Bcf/day from 33.1 Bcf/day last year, which reflects elevating demand and can support prices.

– December started with a short lived cold front but ended with slight above normal temperatures in the eastern U.S. However, there are some indications that January may be colder than previously forecasted.

– Month to date LNG exports level stayed above 14 bcf/day. Consistent growth in exports could indicate growing global demand while tightening domestic supply.

Charts and graphs sourced from Constellation